How to Calculate How Much PMI Mortgage Insurance Will Be

06-06-2024About MortgagesEddie KnoellIn this episode, we’re talking about PMI. PMI stands for Private Mortgage Insurance. PMI, or Private Mortgage Insurance, is associated with conventional loans. This insurance protects lenders when the loan is private and non-governmental.

When is PMI (Mortgage Insurance required?

PMI is required for loans with less than a 20% down payment.

How is PMI Calculated?

PMI rates depend on several factors:

Down payment percentage (e.g., 5%, 10%, 15%)

Loan amount

Number of borrowers

Credit score

Property type

Debt-to-income ratio

PMI on Investment Properties

Technically for Investment properties the minimum down payment is 15%, and in these cases if a borrower puts down only 20% they will have PMI. The issue is, the PMI is extremely expensive and the interest rate could be higher. As a result most investment borrowers put a minimum of 20% down to avoid the extra cost.

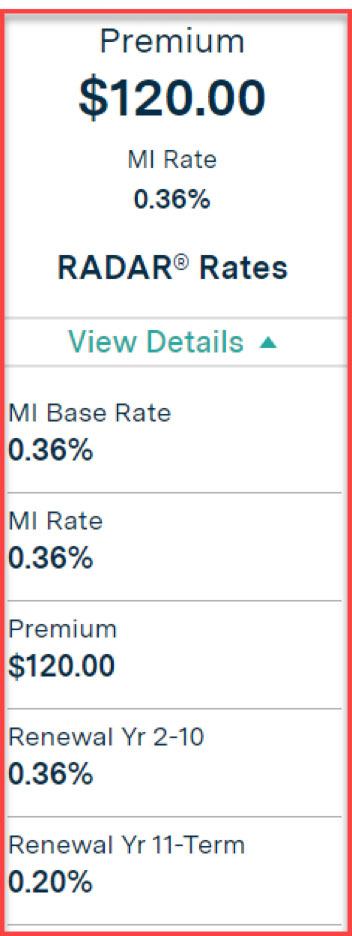

An example quote for Private Mortgage Insurance

Check out this PMI example quote. This is from the private mortgage insurance company, Radian.

When calculating this rate, we put in a 5% down loan, a $200,000 loan amount, one borrower, a 760 credit score, single family residence, and we selected it to be a primary residence. For a $400,000 loan with a 5% down payment, one borrower with a 760 credit score, and a primary residence, the PMI is about $120 per month at a rate of 0.36% (annually divided by 12). This rate may adjust after 10 years, potentially decreasing to 0.2%, though many refinance before reaching this period.

How to remove PMI Mortgage Insurance?

Your monthly PMI payment decreases as your loan amount reduces, although the PMI rate remains constant. There are 2 ways you can have Mortgage Insurance removed;

By law, PMI must be removed when the loan amount reaches 78% of the original value. This should happen automatically, whether you make your scheduled payments or whether you decide to accelerate your principal reductions.

If you have been making online mortgage payments for at least 12 months and you believe your home equity is greater than 20%, you can contact your mortgage lender and petition the mortgage lender to have it removed. The mortgage lender is not obligated to remove it in this case, but often, they will consider removing it. They often will order an appraisal to verify the value and the amount of equity you have in the home. After considering your payment history and equity, they may remove the Mortgage Insurance.

•••

Be sure to ask us for a free quote on your next mortgage. We’ll personally work with you and help you through the whole process.

Signature Home Loans LLC does not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only. You should consult your own tax, legal, and accounting advisors before engaging in any transaction. Signature Home Loans NMLS 1007154, NMLS #210917 and 1618695. Equal housing lender.

BACK TO LIST