Saving For a Down Payment After Graduation

05-23-2017About MortgagesEddie KnoellGrad Season in Arizona – Time to Talk About Planning for Homeownership

Rising prices are pushing down payments higher, while debt loads are a concern for many graduates. Today’s grads and would be buyers must develop positive money habits as early as possible to put homeownership in reach when they are ready to buy.

The graduation season is upon us. Most grads aren’t thinking too much further ahead than saying goodbye to four years on campus and finding their first job. But in a year or two, many of these recent graduates will be thinking about buying their first home. One of the first hurdles they’ll face is pulling together a down payment.

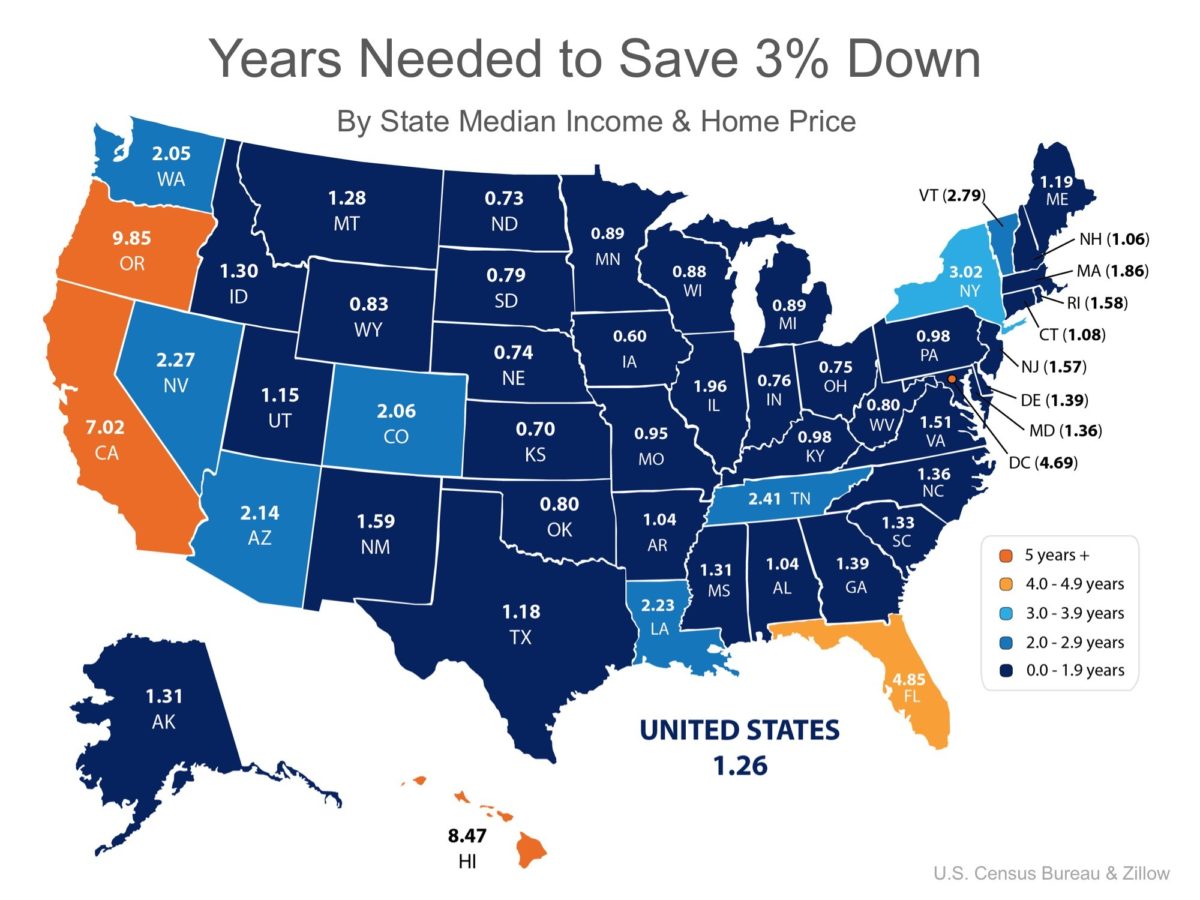

So, how difficult is it for today’s buyers to save enough money to buy a home? Simplifying the Market recently released an infographic indicating that in Arizona, it takes more than seven years to save a 10% down payment assuming an average priced home and average wages. A down payment of 3% takes a little over two years to save.

This might be a bit off-putting to a would-be first time buyer with no savings, but there’s good news in these numbers. For the average buyer, saving enough to get into a starter home is a goal that can be reached in just a few years with careful planning. But it does require planning, which is the message we need to share with our buyers and the recent grads in our lives. Gone are the days when stable income and good credit were enough to get a buyer into their first home. Today’s’ lenders almost universally require a down payment, from 3.5% for FHA on up to 5 – 20% for conventional loans.

One significant exception to the down payment requirement is the VA loan program. But in general, the more a buyer saves, the easier it will be to buy that first home.

For many of our recent college grads, however, saving money is unfamiliar territory. Our advice to them is that now is the time to develop good spending and saving habits. Two of the most important positive money habits they’ll need to develop if they want to be homeowners include:

Minimizing debt – Recent studies indicate that as many as 60% of recent grads have student debt, with average balances of $35,000. And although today’s grads have lower credit card balances and are more likely to pay off their balances than students a decade ago, they are still carrying higher debt loads overall. Paying off student debt and not acquiring new high interest debt on credit cards needs to be a top priority for today’s graduates.

Keeping rates low – Many recent grads don’t understand how interest impacts their finances and may make unwise financial decisions as a result. Every dollar in interest paid reduces the amount of money available to save or spend on other things. Grads should focus on paying off highest interest debt first in order to make their path to savings easier.

Setting realistic goals – Another challenge for many recent grads is understanding that their first home probably won’t be their last. Many buyers start out in smaller, more affordable homes where they can earn equity before moving up into something larger in later years.

By sharing these messages with the recent grads in our lives, we can help them be realistic about what it really takes to buy a home in today’s market. Saving up for the things we really want in life takes financial savvy and maturity, but the post-college years are a great time to begin building these financial muscles.

BACK TO LIST